Business Owner Planning

From succession planning and exit strategies to employee benefits and contingency planning — comprehensive financial guidance built for the unique demands of business ownership.

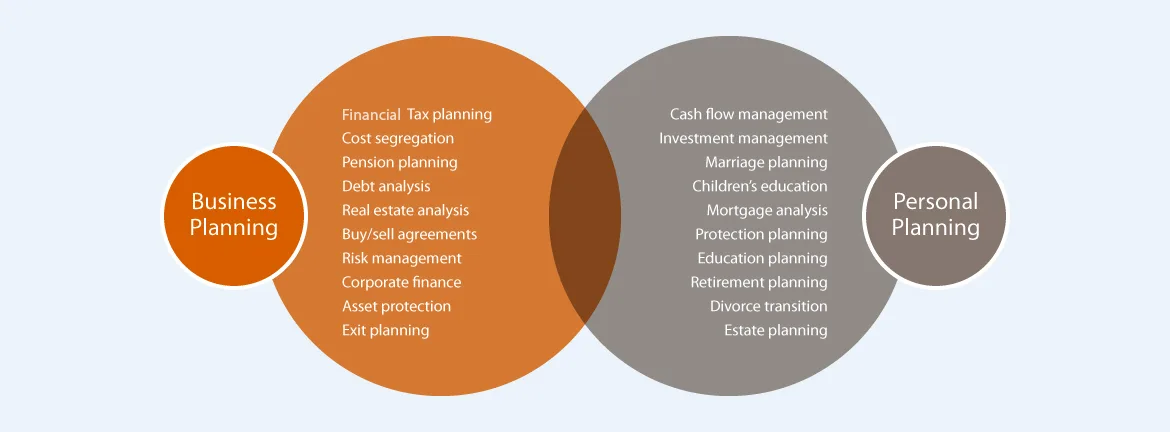

Planning for the future of your business

Successful businesses continually adapt and evolve. Each business owner strives for growth, fresh clientele, and innovation. After years of relentless dedication, you may start contemplating the future trajectory of your business — and that is exactly the moment when proactive planning matters most.

Our team thrives on equipping industrious business owners with pertinent guidance and knowledge. We provide financial strategies along with a plan to transition the business to a successor, facilitating a smooth transition into retirement. We help ensure you have a contingency plan in place in the event of unforeseen circumstances.

Our clients gain access to an extensive network of professionals to aid in successfully realizing both their business and personal objectives — including legal counsel, tax advisors, valuation specialists, and employee benefits professionals, all working in a coordinated fashion around your goals.

A meticulous process for every situation

Recognizing that every situation is unique, G&R Financial Solutions adheres to a meticulously planned process for succession planning. This process includes bringing together all of the business owner's advisors to discuss the following key components — ensuring a coordinated, comprehensive approach to your transition.

Pre-Sale Planning

Business advisory and outlining the crucial steps to prepare your business for sale. We assemble all your advisors — legal, tax, financial, and valuation — to ensure a fully coordinated approach well before a transaction occurs.

Exit Strategies

Formulating strategies for your liquidity event, business exit, and succession planning. Whether selling to a strategic buyer, private equity, family member, or key employee — we model the after-tax outcomes of each path to inform your decision.

Tax Efficient Portfolios

Customized investment and wealth strategies designed to meet your specific wealth objectives, risk tolerance, and future aspirations — ensuring the proceeds from your business exit are deployed in a way that supports your long-term financial independence.

A successful business exit doesn't happen by accident. Owners who engage in proactive succession planning consistently achieve higher valuations, better terms, and a smoother transition into the next chapter of their lives. The earlier you start, the more options you have.

Supporting your team, freeing your focus

At G&R Financial Solutions, we serve as a supportive guide in your journey, allowing you to concentrate on your employees and their welfare. Our approach involves relieving you, the employer, of the burden by stepping in to assist your employees directly.

We navigate you through everything from regulatory compliance and budgeting to strategic planning — while helping your employees comprehend the true value of their benefits and use their programs judiciously. Our goal is for them to recognize that they possess more than just insurance coverage; they have excellent medical, ancillary, and retirement plan benefits working in their favor.

- Regulatory compliance guidance — navigating ACA requirements, ERISA obligations, and plan documentation standards

- Benefits budgeting and cost management — structuring plans that are sustainable for the business and valuable to employees

- Strategic benefits planning — aligning your benefits package with your recruiting and retention objectives

- Employee education and enrollment support — ensuring employees understand and maximize the value of their benefits

- Retirement plan design and oversight — from SIMPLE IRAs and 401(k)s to defined benefit plans for key employees

Frequently Asked Questions

What business owners ask most often about succession, exit planning, and financial strategy.

The ideal lead time for a planned business exit is 3 to 5 years — and ideally longer. This window allows time to increase business value, clean up financial statements, reduce owner dependency, build or document key management, identify and qualify buyers or successors, and structure the transaction for optimal tax outcomes.

During that window, there are specific milestones to hit: obtaining a professional business valuation (and understanding what drives value in your industry), implementing an operating structure that can function without you, establishing a retirement plan robust enough to complement the business proceeds, and working with legal and tax advisors to model the after-tax net from different exit scenarios. Owners who start this process early consistently achieve higher valuations and better terms. If circumstances force an expedited exit — illness, a partnership dispute, an unsolicited offer — the options narrow considerably, but proactive coordination can still make a meaningful difference.

The right plan depends on several factors — your business structure, number of employees, income level, and cash flow patterns. If you're self-employed with no employees and want simplicity, a SEP-IRA or Solo 401(k) are typically the first choices; the Solo 401(k) usually allows higher total contributions. If you have employees, a SIMPLE IRA or 401(k) plan brings them into the equation; the administrative requirements increase, but so does the benefit to your team and your ability to attract talent.

For high-income owners over age 50 who want to shelter the maximum amount possible and have stable, profitable cash flow, a defined benefit or cash balance plan can allow contributions far exceeding the defined-contribution limits. These plans can allow annual contributions of $100,000 or more — sometimes significantly higher for older, higher-earning owners. Business structure also plays a role: an S-corp owner, sole proprietor, and C-corp owner each calculate contributions differently, and optimizing the salary/distribution split can meaningfully affect how much can go into the plan. We work through the specifics to find the structure that maximizes after-tax wealth accumulation for your situation.

A buy-sell agreement is a legally binding contract between business co-owners that governs what happens to an ownership interest when a triggering event occurs — death, disability, retirement, divorce, bankruptcy, or a voluntary desire to sell. Without one, those events can create serious problems: a deceased owner's heirs may have no obligation to sell and no agreed-upon price; a divorcing owner's spouse may become a partner by default; a disabled owner may remain on the books indefinitely without contributing.

The two main structures differ in who does the buying. In an entity-purchase agreement, the business buys out the departing owner's interest. In a cross-purchase agreement, the remaining individual owners buy out the departing owner directly. Cross-purchase agreements typically give surviving owners a higher cost basis in the acquired shares, which can reduce capital gains taxes on a future sale — a meaningful advantage in closely held businesses with significant appreciation.

Regardless of structure, life and disability insurance is almost always the most efficient funding mechanism. It provides the liquidity to execute the buyout exactly when the triggering event occurs, without requiring the surviving owners or the business to scramble for cash at the worst possible moment. If you have a co-owner and no funded buy-sell agreement, this is one of the most urgent gaps in your business financial plan.

Your business built your wealth. A plan protects it.

From your first hire to your final exit, G&R Financial Solutions helps business owners build the financial infrastructure their success deserves.